How many Americans have $1,000,000 in retirement savings? — What the data really says

This article explains the data sources researchers use, why published estimates vary, which groups are most likely to reach $1M inside retirement accounts, and practical retirement planning tips to set realistic, inflation-aware targets. Use the checklist and the simple framework here as a starting point to track your own progress.

What we mean by $1,000,000 in retirement accounts

When people ask how many Americans have $1,000,000 in retirement accounts, it helps to be precise about what counts. In this article I use the phrase retirement-account balances to mean employer plans like 401(k), 403(b), 457 plans and individual retirement accounts such as IRAs, distinct from total household net worth, and I use public survey baselines to explain the differences, including the Federal Reserve Survey of Consumer Finances as the main public reference Survey of Consumer Finances.

Counting only plan balances will give a different answer than counting total household retirement wealth or net worth because some households hold retirement assets outside plans or have significant nonretirement equity and property. That definitional gap is why a single headline number can be misleading when you compare reports. See Investopedia.

For everyday readers, the practical point is simple: check whether a report measures defined-contribution balances, IRAs, total household retirement accounts, or total net worth before you compare numbers across sources; see our personal finance section.

Key datasets and where the numbers come from

The baseline public dataset for household retirement and net worth distributions is the Federal Reserve Survey of Consumer Finances, which researchers and journalists commonly use to estimate how common high retirement balances are Survey of Consumer Finances.

Industry reports from recordkeepers and retirement research groups add complementary views because they focus on plan populations and participant balances; for example, large plan analyses published by retirement recordkeepers show patterns within plan participants that look different from household surveys How America Saves 2024.

Because these sources use different samples and definitions, good comparisons note whether a number refers to plan participants, IRA holders, adults, or households, and whether it is nominal or inflation-adjusted.

Headline finding: how many Americans have $1,000,000 in retirement accounts

Major public and industry analyses tend to cluster in a low single-digit share for $1,000,000 or more held specifically in retirement accounts, with many reports pointing toward a range roughly between 2 percent and 4 percent, depending on the sample and definition How America Saves 2024. See also Yahoo Finance.

Compare your accounts with a consistent checklist

Use the practical checklist later in this article to see how your accounts compare to consistent targets, and review the definition you choose before making decisions.

Learn about FinancePolice advertising options

That low single-digit pattern is visible across matched analyses because higher balances tend to cluster in a minority of households. Short-term market moves and the timing of a survey can shift those shares up or down, which is why year-to-year comparisons need the same account definitions to stay useful The State of Millionaire Households and Retirement Savings.

When reading a headline about percent with $1M, note whether the number refers to adults, to households, or to active plan participants; those frames produce different percentages even from the same raw data.

Why estimates vary: definitions, samples, and timing

One main reason estimates differ is simple definition: some reports count only defined-contribution plan balances, while others add IRAs or try to capture total household retirement wealth, and those choices change the headline share Retirement Confidence and Account Distribution methodology notes.

Another source of variation is sample frame. A report of plan participants excludes nonparticipants and can be biased toward those already saving, whereas household surveys try to include everybody but use weighting and top coding that affect how the largest balances are represented Survey of Consumer Finances, and you can consult our how-to-budget guide for tracking inflation-adjusted targets.

Timing matters too. Estimates based on market values reflect recent gains or losses, so a strong market run raises reported shares of $1M+ accounts and a market downturn lowers them, at least until new survey microdata are collected and released The State of Millionaire Households and Retirement Savings.

Age, income, and who holds most retirement assets

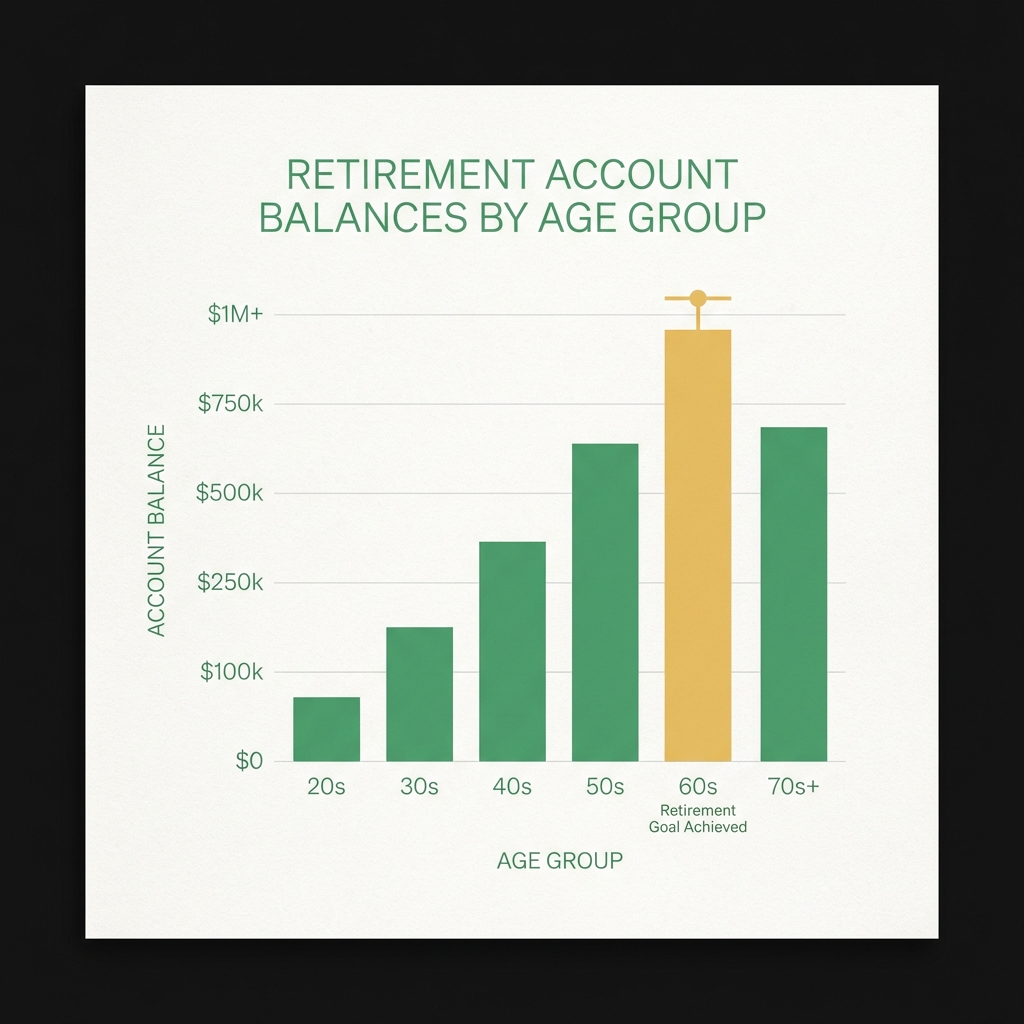

Evidence from recordkeepers and retirement studies shows that higher retirement balances are much more common among older households and top earners; the likelihood of $1M+ balances rises with age and income in most reports How America Retires 2024.

Older age groups, often those nearing or in early retirement, are more likely to have accumulated larger balances because they had a longer time horizon to save and benefit from compound returns; similarly, high earners save more in absolute dollars so they represent a disproportionate share of million-dollar accounts Who Holds Retirement Assets?.

Estimates from major public and industry sources show that $1,000,000 or more held specifically in retirement accounts is uncommon and typically present in a low single-digit share of households or adults; the exact percentage depends on definitions and samples.

These patterns mean aggregate retirement assets are concentrated: a minority of households hold a majority of plan balances, which skews the distribution and makes $1M more common in that subgroup than in the population as a whole Survey of Consumer Finances.

How to read recordkeeper reports versus household surveys

Recordkeeper reports typically describe plan participants and plan balances, often excluding rollover IRAs, nonparticipants, and other household assets; they are useful for understanding what active savers have inside employer plans How America Saves 2024.

Household surveys like the SCF aim to capture total household assets and liabilities across all account types, but they use sample weighting, top coding, and other statistical adjustments that change how the largest balances are represented, so you may see fewer very large accounts in the public microdata than in private plan-level reports Survey of Consumer Finances.

Practical advice: compare like with like. If a report says X percent of plan participants have $1M+, do not treat that X as equal to the percent of households with $1M in all retirement accounts.

What this means for retirement planning tips: a simple framework

Start by picking a clear definition to track. Decide whether you will measure retirement-account balances only or total retirement wealth including IRAs and taxable investments; write that definition down and use it consistently over time Survey of Consumer Finances.

Measure targets in inflation-adjusted terms and review progress at regular intervals, such as annually, rather than reacting to short-term market swings The State of Millionaire Households and Retirement Savings.

account inventory and annual review template

Use annually

Basic practical steps that tend to help most savers include steady contributions, taking full employer match when available, maintaining a diversified mix, and keeping fees low where possible. Use the checklist tool above to record what you include in your definition before comparing yourself to published statistics.

These are retirement planning tips that focus on consistency and clarity rather than chasing a single headline number.

Practical checklist to assess your own progress

Start an account inventory. List each retirement account by type, include IRAs and employer plans if you decided to count them, and note current balances and contribution rates so you have a consistent baseline for tracking How America Saves 2024.

Set simple annual benchmarks. For example, record your inflation-adjusted balance each year, compare percent funded against an age-adjusted target you choose, and track whether you are saving the percent of income you planned to save.

Document assumptions such as intended retirement age, expected withdrawal strategy, and whether you include pensions or Social Security in your target-this keeps comparisons meaningful year to year.

Common mistakes people make when judging million-dollar retirement goals

A frequent mistake is mixing total net worth and retirement-account balances. A household may have a $1M net worth because of home equity or taxable investments while holding far less inside retirement accounts, so be clear about which measure you use Survey of Consumer Finances.

Another common error is ignoring taxes, fees, and inflation. A nominal $1M balance will buy less over time if you do not adjust for inflation, and taxes or high fees can substantially change net retirement income, so translate balances into realistic after-tax cash flow before deciding a target The State of Millionaire Households and Retirement Savings.

Finally, be aware of sampling and survivorship biases in some reports that make large balances look more common among specific samples than they are in a population-wide household survey.

Scenarios: typical paths and timelines people follow

Younger savers who start early and save a steady percent of income often have more time for compound growth, but they usually do not reach $1M until midcareer or later unless they have very high savings rates or early windfalls How America Retires 2024. See The Motley Fool.

Midcareer earners increase the chance of reaching $1M if they raise contributions, capture employer matches, and keep costs low; progress depends heavily on career earnings, savings rate, and market returns during the accumulation period How America Saves 2024.

Near-retirement households with larger balances reflect decades of saving or higher lifetime earnings; these groups tend to account for a disproportionate share of reported $1M+ balances in many studies Who Holds Retirement Assets?.

Adjusting targets for inflation, taxes, and lifestyle

Nominal balances do not equal purchasing power. Convert a $1M nominal target into an inflation-adjusted target based on your expected retirement date so you know what level of spending it supports in todays dollars Survey of Consumer Finances.

Account types and tax treatment matter. Withdrawals from traditional pre-tax accounts are taxable while Roth accounts can provide tax-free income, so the same nominal balance can produce different after-tax retirement income depending on the account mix The State of Millionaire Households and Retirement Savings.

Also reflect personal lifestyle choices and longevity in your assumptions. Two households with the same $1M may plan very different spending paths depending on health, desired travel, housing, and whether they expect significant legacy transfers.

How to use public data to track changes over time

Full SCF documentation and periodic summaries are available from the Federal Reserve and remain the primary public source for household retirement and net worth distributions; use those releases to anchor long-term comparisons Survey of Consumer Finances.

Recordkeeper and industry reports appear more frequently and can show short-term shifts among plan participants, but remember they may not capture IRAs or households outside employer plans, so always check definitions when a new report is released How America Saves 2024.

Because public microdata after 2022 are limited, watch for new releases and read the methodology notes carefully before treating a single-year change as a trend Survey of Consumer Finances.

Questions to ask a plan provider or financial professional

When you review plan or account summaries, ask which accounts are included, whether rollover IRAs are counted, and which fees are deducted from reported balances so you understand the coverage and the basis of reported numbers Retirement Confidence and Account Distribution methodology notes.

Also ask whether historical numbers are nominal or inflation-adjusted, and request a simple export of your account balances and contribution history so you can apply the same definition you use when comparing public statistics.

Summary and realistic next steps

In short, holding $1,000,000 specifically in retirement accounts is uncommon in the United States and tends to be concentrated among older and higher-income households; reported shares are usually in the low single-digit range when measured carefully.

Set a clear, inflation-aware definition and track your progress with an account inventory, annual reviews, and steady contribution habits. Use primary sources and consistent definitions when you compare yourself to published numbers and update assumptions as new public data arrive. See our guide on financial freedom and financial independence.

No. A $1,000,000 net worth can include home equity and taxable investments, while $1,000,000 in retirement accounts refers only to balances in retirement-specific accounts like 401(k)s and IRAs.

Researchers commonly use the Federal Reserve Survey of Consumer Finances for household distributions and compare it with industry reports from large recordkeepers to see patterns among plan participants.

Create an account inventory listing each retirement account and contribution rate, choose whether to include IRAs and taxable investments, and review your inflation-adjusted balance annually.

If you want to compare yourself to public statistics, pick a definition, document it, and use the checklist in this article to update your plan each year.

References

- https://www.federalreserve.gov/econres/scfindex.htm

- https://institutional.vanguard.com/content/dam/inst/pdf/HowAmericaSaves_2024.pdf

- https://financepolice.com/advertise/

- https://www.investopedia.com/retiring-with-1-million-is-rare-heres-how-many-people-actually-do-it-11869328

- https://financepolice.com/category/personal-finance/

- https://finance.yahoo.com/news/many-americans-retire-coveted-1-121100983.html

- https://www.pewresearch.org/social-trends/2025/07/10/millionaire-households-retirement-savings/

- https://www.ebri.org/docs/default-source/rcs/rcs_2024.pdf

- https://financepolice.com/how-to-budget/

- https://www.fidelity.com/bin-public/060_www_fidelity_com/documents/retirement-savings-report-2024.pdf

- https://www.nirsonline.org/wp-content/uploads/2024/04/retirement-asset-distribution-2024.pdf

- https://www.fool.com/money/buying-stocks/articles/how-many-people-really-save-1-million-for-retirement-2/

- https://financepolice.com/financial-freedom-and-financial-independence/

You May Also Like

XRP-linked Ripple rolls out treasury platform after $1 billion GTreasury deal

Copy linkX (Twitter)LinkedInFacebookEmail

The U.S. Has Not Been Taken Advantage Of Since WWII

‘Great Progress’: Cardano Founder Shares Update After CLARITY Act Roundtable

Read the full article at coingape.com.